The Present We Didn’t Ask For

by Jason D. Norris, CFA Executive Vice President of Research

Merry Christmas You Filthy Animal

– Home Alone 2, Lost in New York – 1992

That’s how equity investors received the Federal Reserve’s rate hike and comments earlier this week. While expectations were for the Fed to raise the federal funds rate by 0.25 percent, there was a small glimmer of hope that they may hold pat. There was also a perception by some on the Street that the Fed was on “autopilot,” which if one looks at 2018, as well as the comments from Chairman Powell, this is not the case. We believe that the Fed will be “data dependent” and does not have a preset course for balance sheet reduction or pace of rate hikes. 2018 is a good example of that belief. A year ago, the Fed was expected to raise the funds rate three times in 2018; however, due to the stimulus of the tax cut and fiscal spending, they ended up hiking rates four times. Fed Governor John Williams stated today on CNBC that the Fed will be flexible and that there isn’t a predetermined course regarding interest rate hikes and the reduction of the balance sheet.

That’s the Gift that Keeps on Giving the Whole Year

– National Lampoon’s Christmas Vacation — 1989

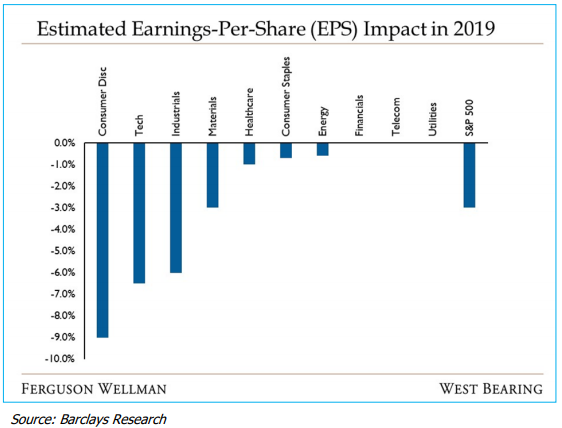

While trade took a backseat to Fed headlines this week, it continues to be an overhang. The periodic headlines, both on the positive and negative front, have increased volatility in the markets due to the uncertainty it has created. Currently, tariffs have focused industrial companies, such as Caterpillar and John Deere. This has been seen primarily in the steel and aluminum tariffs. As we’ve written recently, while the tariffs garner high levels of uncertainty, the actual dollar impact on the economy is relatively small. When looking at the equity markets, if there is a full-blown trade war with China, the effects will spill over to the consumer. Barclay’s highlights below the effects on earnings for each of the 10 economic sectors, as well as the S&P 500. With increased tariffs on Chinese goods, the largest impact is going to be on retailers in the consumer discretionary sector.

The biggest wildcard is the effect a trade war would have on consumer spending. With retailers potentially feeling a big impact, will they raise prices to offset tariff costs, forcing consumers to feel the burden?

Don’t Bother Me … I’m Thinking

– A Christmas Story – 1983

With the recent carnage in the markets and increased uncertainty, investors have to stay disciplined and not get emotional. We understand that volatility can be unnerving; however, we have to stay focused on the fundamentals. We do realize that volatility and uncertainty can persist and we have been making tactical adjustments accordingly. Over the last few months, we have been reducing risk in client portfolios, shifting from highly cyclical sectors into those that are more defensive. We have not, however, begun to sell stocks and add to bonds.

Week in Review and Our Takeaways

• Stocks finished the week falling over 7 percent as investors reduced risk assets in the face increased uncertainty. The Dow Jones Industrial Average suffered its worst week since October 2008

• Questions about Fed policy, continued trade issues and chaos in D.C. have left this month on pace to be the worst December since 1931

• Investors are nervous about Fed policy in 2019 and will lead to continued volatility

• The U.S. economy remains healthy and while we have pared back risk, we are not reducing equity exposure

Tagged: Ferguson Wellman Capital Management, West Bearing Investments, Jason Norris, CFA, Federal Reserve, Federal Funds Rate, Chairman Powell, China, Trade, Volatility

https://www.fergusonwellman.com/fw-team/jason-norris-cfa

F E R G U S O N W E L L M A N

(503) 226-1444 |

(800) 327-5765 W E S T B E A R I N G

(503) 417-1444

A D D R E S S 888 Southwest Fifth Avenue, Suite 1200 Portland, Oregon 97204

Advertisement