PBCO Financial Corporation Reports Q4 and 2022 Earnings

PBCO Financial Corporation (OTC PINK: PBCO), the holding company (Company) of People’s Bank of Commerce (Bank), announced today its financial results for the fourth quarter of 2022 and for year-end 2022.

Highlights

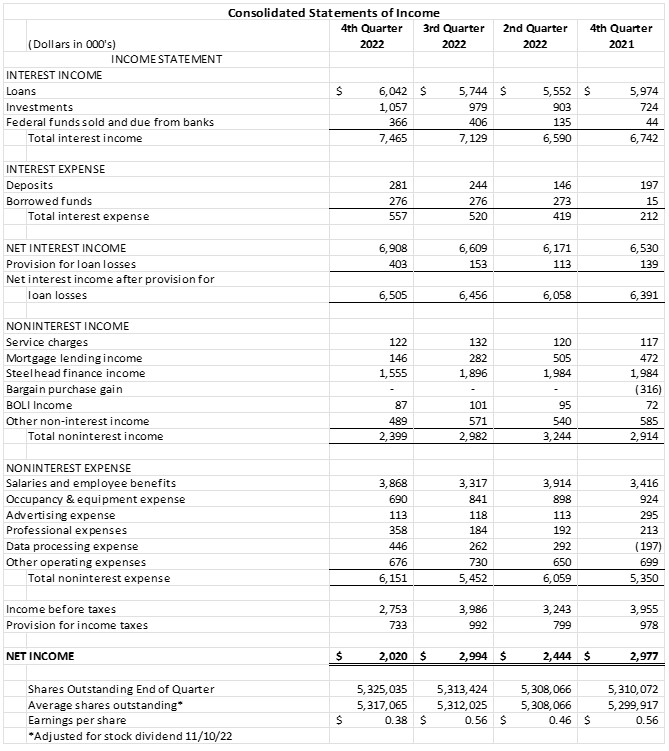

- Net income of $2.0 million in the quarter, or $0.38 per diluted share

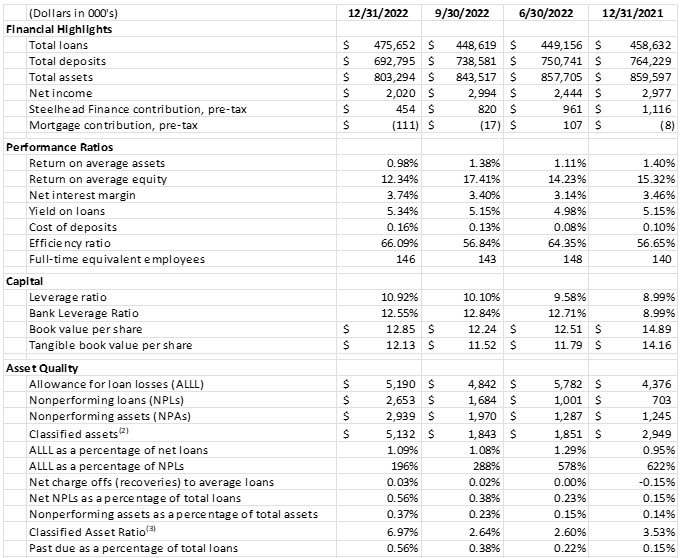

- Loan growth of $27.3 million in the quarter, an increase of 6.1% compared to Q3 2022

- Net interest margin of 3.74%, an increase of 34 basis points compared to Q3 2022

- Cost of deposits was 0.16%, an increase of 3 basis points compared to Q3 2022

- Hired team of commercial bankers in Eugene, Oregon

- Net income of $9.9 million for 2022 year-end, or $1.92 per diluted share

The Company reported net income of $2.0 million, or $0.38 per diluted share, for the fourth quarter of 2022 compared to net income of $3.0 million, or $0.56 per diluted share, in the same quarter of 2021. Earnings for the full year 2022 were $9.9 million or $1.92 per share, down from $11.5 million or $2.33 per share for 2021. The reduction in earnings in 2022 is due to lower mortgage income of $1.7 million and absence of PPP fee revenue, which was $4.7 million in 2021, coupled with one-time income and expenses related to the merger with Willamette Community Bank in March 2021.

“Despite a challenging operating environment in 2022, the Company proved resilient with strong profitability in fourth quarter and full year 2022,” commented Ken Trautman, Chief Executive Officer. “Further, we continue to identify opportunities to grow the Bank and remain focused on serving our customers and delivering strong financial results for shareholders. We recently hired a team of commercial bankers to lead our expansion into Eugene, Oregon, and believe we are well positioned to take advantage of growth opportunities in this market.

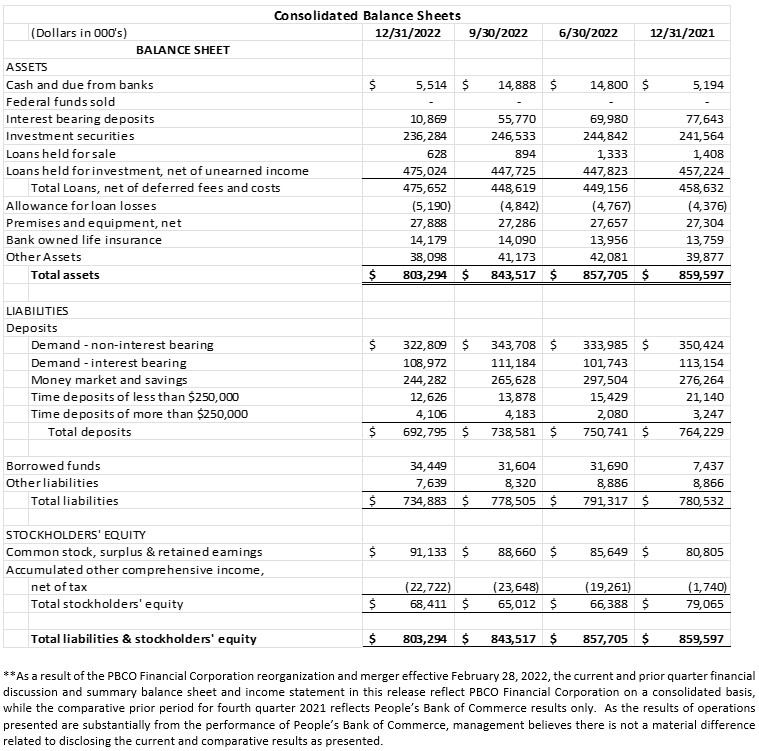

Deposits decreased $45.8 million in the quarter, a 6.2% decline from the third quarter of 2022. Over the last twelve months, deposits decreased $71.4 million, a decline of 9.3%. “A core strength of the Bank is the deposit mix with non-interest bearing balances accounting for 47% of total deposits at year-end,” commented Joan Reukauf, Chief Operating Officer. “We maintained a low cost of deposits at 0.16% for the fourth quarter, but total deposit balances declined in the quarter as some customers sought higher yielding rates in alternative investments.”

Loans increased $27.3 million in the quarter, or 6.1% growth compared to the third quarter of 2022. “We saw higher loan growth in fourth quarter than prior quarters in the year, as we remain focused on quality loan production at attractive rates,” commented Julia Beattie, President. “The Bank had relatively muted loan growth in the first nine months of the year due to our decision to remain disciplined when loans were at historically low interest rates.”

The investment portfolio decreased $5.3 million or 2.2% from the fourth quarter of 2021. During the most recent quarter, investments decreased $10.2 million from the third quarter of 2022, or 4.2%, and the average life of the portfolio remained at 4.6 years as short-term investments matured and were not replaced. Securities income was $1.06 million during the quarter, a yield of 1.7%, versus $979 thousand or a yield of 1.5% for the third quarter of 2022.

Non-performing assets increased in Q4 as total loans past due or on non-accrual increased to 0.56%, as a percentage of total loans, versus 0.38% as of Q3 2022. “The Bank’s overall asset quality remains strong, but we did see an increase in non-performing assets for the quarter. This increase was due to a hospitality credit that has not fully recovered from the pandemic shutdown,” noted Bill Whalen, Chief Credit Officer. During the fourth quarter, the Allowance for Loan and Lease Losses (ALLL) increased by $348 thousand due to new loan growth as well as net charges offs of $56 thousand during the quarter. As of December 31, 2022, the ALLL was 1.09% of portfolio loans and the unallocated reserve stood at $839 thousand or 16.2% of the ALLL.

Fourth quarter 2022 non-interest income totaled $2.4 million, a decrease of $583 thousand from the third quarter of 2022. During Q4 2022, Steelhead Finance factoring revenue decreased $341 thousand, an 18.0% decrease from the prior quarter, while increasing $774 thousand year-over-year, or 11.6%. “A majority of revenue generated by Steelhead Finance comes from our factoring partnerships in the freight industry,” commented Bill Stewart, Steelhead Division President. “The spot market freight surge, which yielded record freight margins in 2021 and into 2022, came to an end in the fourth quarter of 2022 and has returned to a more normalized level as reflected in Q4 revenue,” added Stewart. Increased mortgage rates in 2022 led to a significant decrease in mortgage production, and consequently, mortgage income decreased $136 thousand, or 48.2%, from the third quarter of 2022 and decreased $1.7 million, or 54.9%, for full year compared to 2021. Additionally, the Bank had a non-recurring one-time bargain purchase gain of $1.7 million from its merger with Willamette Community Bank in March of 2021 that inflated non-interest income during 2021.

Non-interest expense totaled $6.2 million in the fourth quarter, up $699 thousand from the previous quarter. The primary reason for the increase in expense was attributed to salaries and personnel benefits due to an accrual adjustment. On an annual basis, salaries and benefits were up $1.2 million, a 9.1% increase over 2021. Advertising expense was down $1.0 million compared to prior year as the Bank made a one-time donation in 2021 to provide housing relief for the survivors of the 2020 Alameda Fire in Jackson County. In addition, the Bank incurred one-time merger related expenses of $2.5 million during 2021.

As of December 31, 2022, the Tier 1 Capital Ratio for PBCO Financial Corporation was 10.92% with total shareholder equity of $68.4 million. During the quarter, the Company was able to augment capital through earnings while assets also decreased due to lower deposit balances. The Tier 1 Capital Ratio for the Bank was 12.55% at quarter-end, down from 12.84% as of September 30, 2022. The Company had unrealized losses on its investment portfolio, net of taxes, of $22.7 million down from $23.6 million the prior quarter. “The Bank has a very strong capital position that continues to be well above the threshold to be considered well-capitalized, which was augmented by a successful sub debt offering in March of 2022 totaling $25 million,” commented Lindsey Trautman, Chief Financial Officer.

About PBCO Financial Corporation

PBCO Financial Corporation’s stock trades on the over-the-counter market under the symbol PBCO. Additional information about the Company is available in the investor section of the banks website.

Founded in 1998, People’s Bank of Commerce is a full-service, commercial bank headquartered in Medford, Oregon with branches in Albany, Ashland, Central Point, Grants Pass, Jacksonville, Klamath Falls, Lebanon, Medford, and Salem, with a loan production office in Eugene.

By Press Release

https://www.peoplesbank.bank/about/press-release—january-25-2023

Advertisement