Keep Your Eye On The Ball

By Tim Duy, Senior Director, Oregon Economic Forum, Professor of Practice

A better than expected labor report supported another leg up for Wall Street as it was the latest piece of evidence that the worst of the downturn is behind us. While that is most likely true, note that there are crosscurrents in the economy that make it difficult to discern yet the extent of the damage wrought by the virus-related shutdowns. We will continue to struggle with the the levels versus differences problem for quite some time. The main trap to avoid is that while the “levels” people will be correct and the economy remains stuck in a sub-par growth path, this observation will probably do little to quell the euphoria on Wall Street.

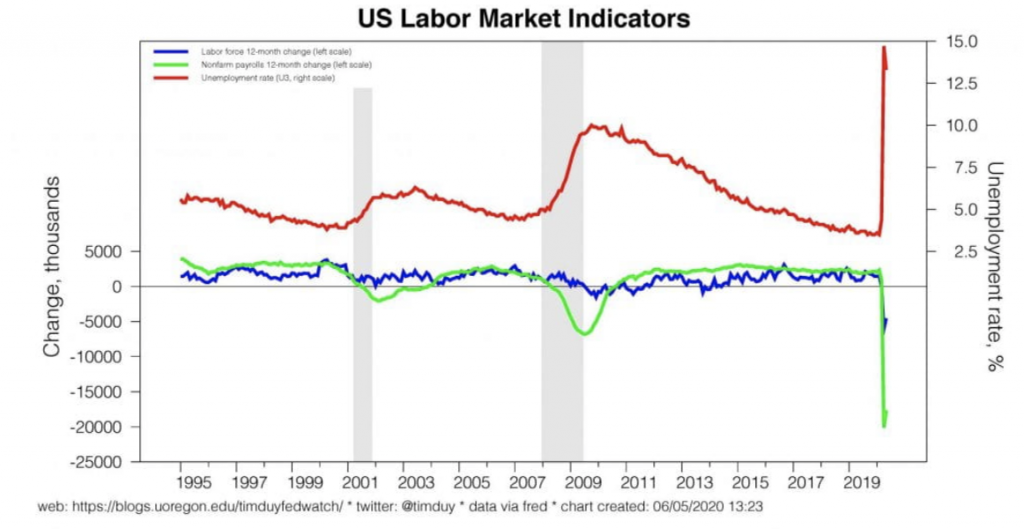

The employment report surprised massively on the upside as the economy added 2.5 million jobs rather than losing 7.5 million as Wall Street expected. The unemployment rate actually fell, with the U-3 headline number dropping from 14.7% to 13.3% and the broader U-6 number falling from 22.8% to 21.8%. Not great by any measure, but suggestive that we shouldn’t obsess over worse-case scenarios.

The jobs gain appears difficult to reconcile with the ongoing large scale layoffs reported via initial unemployment claims and the still high levels of continuing claims. I think the surprise jobs gains reflects the cross-currents in the economy. One current is the reversal of a portion of the initial job losses from the shutdown. Remember, that part of this recession was unlike previous recessions. We engineered a sudden stop in the economy and it was inevitable that when the economy began to reopen, some jobs, many even, associated with that sudden stop would return quite quickly.

Of course, not all of those jobs will quickly return, or return at all. Any activity dependent on large, densely-packed crowds will need to learn to grow around the virus; that will require some time to accomplish. Some may initially come back as part-time rather than full-time. But many are coming back and can do so quickly.

Against this positive current, however, is an opposing force. The hit to demand triggered more typical-recessionary dynamics. Firms not impacted directly by the initial shock still suffer secondary and tertiary impacts that show up as layoffs or hiring freezes that reduce the uptake of workers. Note that those subsequent impacts are of decreasing magnitude; if they weren’t, any initial shock to demand would drive the economy to zero.

What’s likely happening is that the initial impact is reversing in a big way even as the secondary and tertiary impacts are just getting started. It’s a tug of war in the labor markets and that initial reversal won in May.

That’s good news! And it probably foreshadows other good news such as surging retail sales numbers, for example, in the days ahead. But it doesn’t mean a V-shaped recovery overall is in the making. How these opposing forces sort themselves out won’t become evident until later in the year, probably the fourth quarter. But the ultimate level of the economy later this year is less important for financial markets than just being above the bottom. And that looks likely.

Of course, there are some risks to watch for. We need to avoid the W in the recovery; a set-back does not appear to be priced into equities. One of those risks is the impending fiscal policy cliff when the enhanced unemployment benefits expire at the end of July. Congress can fix that risk easily should they not get overly optimistic about the recovery. It is easy to see that another round of fiscal support to cushion activity as the employment dynamics play out could push stocks to all time highs. It’s also easy to see stocks struggle if Congress waivers on another round of aid.

Another risk is a surge in Covid-19 cases that pushes the economy into lockdown mode. We see cases rising in parts of the nation and there is a concern that the ongoing protests will fuel further spread. In the past I was concerned that further spread of the virus would trigger a fresh lockdown. I hesitate on that now. I don’t think it will be easy to push people back inside again. More likely is that any future responses will be more targeted – see Greg Ip at the Wall Street Journal. We didn’t defeat the virus with the initial lockdowns. Instead we bought some time to learn to live with it. Hopefully we learned enough.

Bottom Line: The economy is bouncing off the bottom and a lot of big numbers are going to be bouncing around with it. It’s going to be like watching the ball in a pinball machine as it jerks from one direction to another. Sometimes its hard to keep your eye on the ball its moving so fast. Wall Street is probably going to be satisfied as long as the ball is moving in generally the right direction, which seems the most likely outcome and even more likely if fiscal policy is not abandoned quite yet.

Advertisement