Economic Outlook: On the QT … But QT may not be so quiet this time

Commentary by Robert Whelan, ECONorthwest

DECEMBER 2018

“On the QT,” a quintessentially American phrase. It means to keep something confidential. Basically, QT is an abbreviation for “quiet.” But there is a new meaning and you will be hearing it more and more in the coming months. This time it will mean anything but quiet. The new definition? ‘Quantitative tightening’.

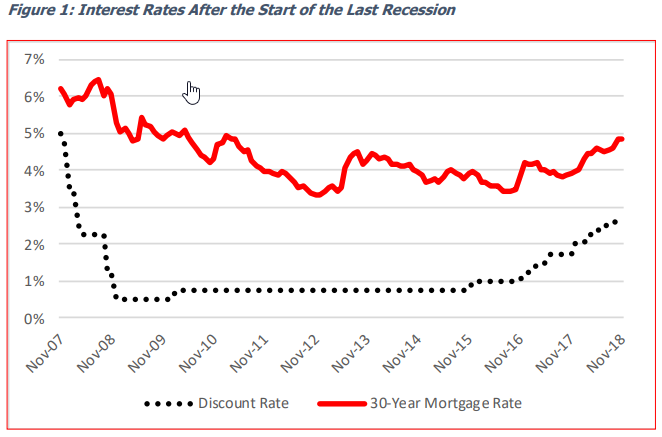

QT is the opposite of quantitative easing (QE). You may recall that in December 2008 we were a year into a deep recession. The Federal Reserve Bank (Fed) had slashed the discount rate (the short-term interest rate it controls) to 0.5 percent. But the economy, especially housing, kept weakening. Foreclosures were happening right and left. The problem was that long-term interest rates, which the Fed doesn’t directly control, stayed persistently high. The rate on a 30-year mortgage then was 5.5 percent. They chose to do something radical. An experiment called QE.

Under QE, the Fed bought bonds and mortgage backed securities by essentially printing new money. The goal was to drive down long-term interest rates so to compel investors to buy riskier investments. That would lift stock market and housing prices, which, in turn would increase the wealth of consumers.

It worked. Long-term rates fell. The 30-year mortgages fell to 3.3 percent in just four years. People refinanced, and others were able to stave off foreclosure, tamping down panic selling. QE kept the foreclosure crisis from getting worse. It also pushed up other asset prices such as land, stocks, and even artwork. Corporations too were able to borrow cheaply. And borrow they did.

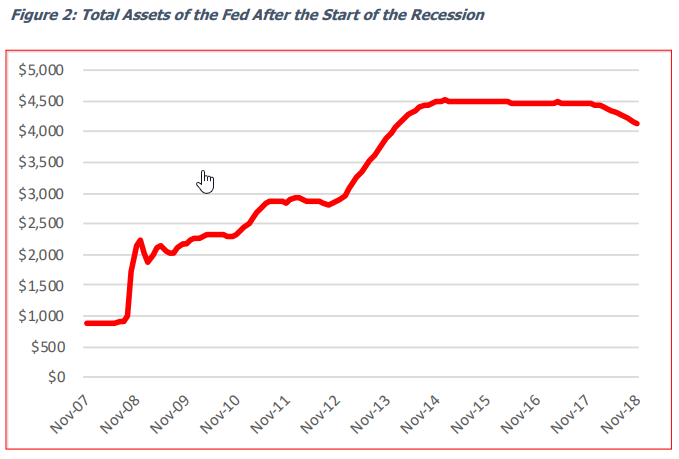

The Fed didn’t stop after four years. When they tried to the economy would falter. Ten years into QE the Fed’s holdings of bonds and mortgage-backed securities went from $882 billion to nearly $4.5 trillion — a five-fold increase well in excess for the economy’s size. QT is a way of taking the excess out.

1. Bhar, A.G. Malliaris, and M. Malliaris. “Quantitative Easing and the U.S. Stock Market: A Decision Tress Analysis.” Review of Economic Analysis. July 2015. Pp. 135-156.

2. S. Gabriel and C. Lutz. “The Impact of Unconventional Monetary Policy on Real Estate Markets.” Federal Reserve Bank of San Francisco. November 10, 2017.

3. C Fried. “Quantitative Easing Kept the Foreclosure Crisis from Being Even Worse.” UCLS Anderson Review. July 25, 2018.

4. Williamson, Steven. “Quantitative Easing: How Well Does This Tool Work?” Regional Economist. Third quarter 2017. Federal Reserve Bank of St. Louis.

5. M. Cosgrove. “The Fed seems determined to snuff out economic progress.” The Hill. October 19, 2018.

Today the economy is running hot with rising inflation, excess speculation, and high-risk companies issuing junk bonds with abandon. And so begins the slow process of the Fed trying to get things back to normal. They’ve started the second half of their economic experiment: QT. Rather than buy new bonds with money they got when old bonds in the Fed portfolio matured, they are simply withdrawing money out of the economy. They will drain about $600 billion dollars out over the year. Other central banks in the world are following.

How will this pan-out? Nobody really knows. But long-term rates are already rising and are likely to continue rising. That would hurt real estate prices among other investment asset prices. As reported recently in The Economist, high housing prices have less to do with supply shortages and more to do with financial markets where QE pushed rates down. Then there is excess corporate debt, which is now near record highs and vulnerable to rising rates.

The risks are great. The Fed admits as much saying, “elevated valuation pressures imply a greater possibility of outsized drops in assets prices.” “Excessive borrowing by businesses and households leaves them vulnerable to distress if their incomes decline or the assets they own fall in value.” And, “financial institutions will not have the ability to absorb even modest losses when hit with adverse shocks.”

Some believe the Fed is underestimating the risks. Benn Steil and Benjamin Della Rocca of the Council of Foreign Relations were quoted in Barron’s saying that QT has already added 17 basis points to the benchmark 10-year Treasury bond and that “Monetary policy will start to contract economic growth early next year.” A year ago, I forecast a possible recession by the end of 2019.

There are counter arguments. This is economics after all. It’s possible to slow the pace of tightening. That would take pressure off the economy and let consumer and business spending grow a bit faster. But if Fed cuts back tightening too much, inflation will worsen and that comes with a whole set of new problems.

6. “There is more to high housing prices than constrained supply.” The Economist. November 24, 2018. P. 65.

7. “C. Torres and A. Tanzi. Corporate America’s debt boom looks like a bust for the economy.” Bloomberg. November 18, 2018.

8. “Financial Stability Report.” Board of Governors of the Federal Reserve System. November 2018. Pp. 3.

9. R. Forsyth. “Will the Fed Back Down?” Barron’s. November 26, 2018. P. 5.

10. R. Whelan. “Running out of fuel.” Economic Outlook. September 2017.

Even the Fed says this won’t be easy, calling the process “threading the needle.” We will know in the fullness of time if QT will indeed be quiet or be something much more disquieting. In the meantime, it may be wise for all of us to be prudent and avoid taking big risks with our money and savings.

Robert Whelan Director

ECONorthwest

222 SW Columbia, Suite 1600,

Portland, OR 97201

Advertisement